Case Name: Actuarial Employee Benefit Claims Allowed; ITAT Deletes Large Expense Additions

- Appeal Number: ITA No.5756/Mum/2025

- Date of Judgement/Order: 08/04/2026

- Related Assessment Year: 2017-18

- Courts: ITAT Mumbai

-

Read More

Download

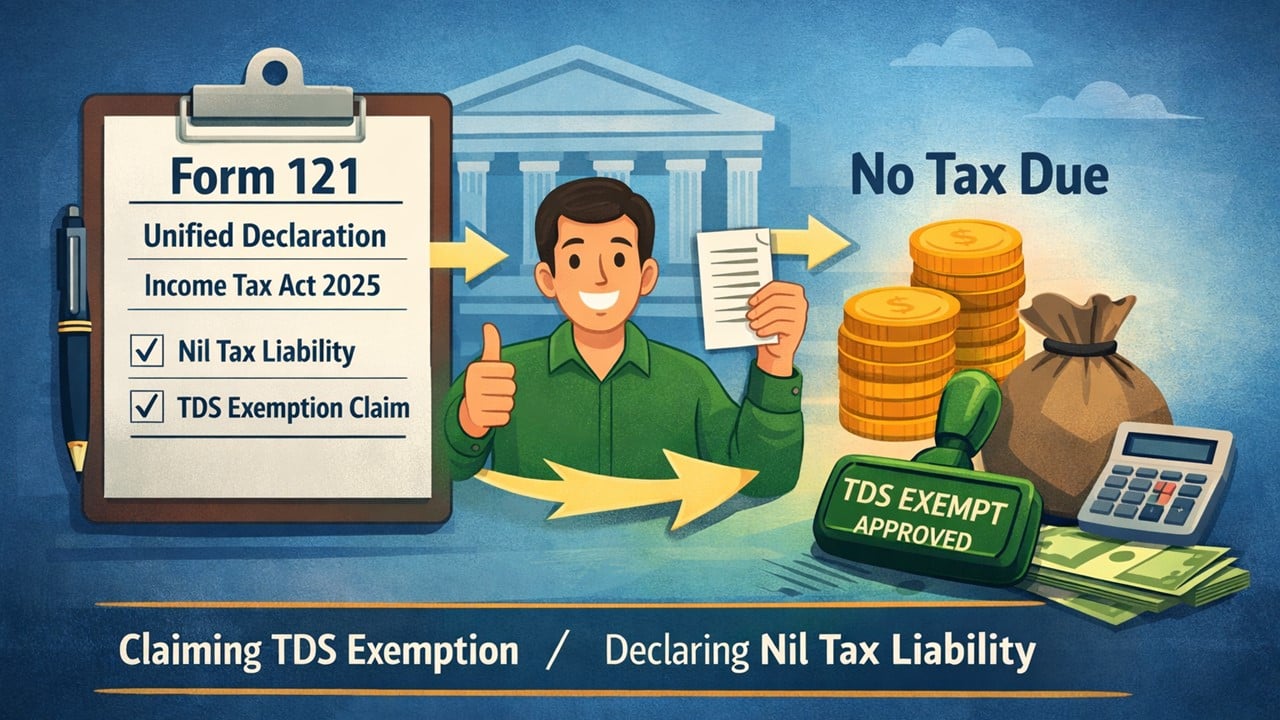

Case Name: EPFO releases clarification for transition from Income Tax Form 15G/15H to unified Form 121

- Appeal Number:

- Date of Judgement/Order:

- Related Assessment Year:

- Courts:

-

Read More

Download

Case Name: Substantial Justice Should be Preferred Over Technical Delay in Appeal Filing: ITAT

- Appeal Number: ITA No.9073/Mum/2025

- Date of Judgement/Order: 10/04/2026

- Related Assessment Year: 2016-17

- Courts: ITAT Mumbai

-

Read More

Download

Case Name: ITAT Quashes Assessment Passed in Name of Non-Existent Amalgamated Company

- Appeal Number: ITA No. 5793/Del/2024

- Date of Judgement/Order: 10.04.2026

- Related Assessment Year: 2021-22

- Courts: ITAT Delhi

-

Read More

Download

Case Name: Rs 22 Crore Fake ITC Scam: Panipat Youth Denied Bail in Bogus Firm Network Case

- Appeal Number:

- Date of Judgement/Order:

- Related Assessment Year:

- Courts:

-

Read More